Highlight:

2015 was a miserable year for Stainless Steel Manufacturers in Asia as their exports were curbed by trade cases and the overall demand also shrank. But 2016 proved to be much better for the suppliers, mainly the Chinese ones. Contrary to the pattern in Europe, there is an increase in demand of Austenitic Stainless Steels and it is estimated that the conversion margins for suppliers of the same will rise this year. It has also been seen that the producers who were used to see large gains in demands, decided to voluntarily reduce production in 2016 when margins were clearly poor. Thus, if the demand growth goes slow this year, it is suspected the margins will fall even if raw materials push the prices higher.

Margins dipped in December, now on their way up again

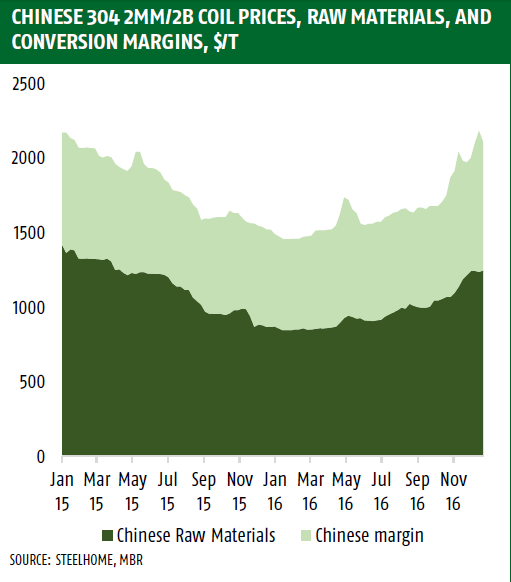

It was expected that the Chinese domestic market prices were to dip unless the export market prices were to pick up. The prices reached a 2-year high in November when the spot prices for grade 304 coil reached about $2000/ton, but after that, the downturn resumed. This downturn occurred precisely at the same time as the raw material prices were on the rise. In fact, the prices of local nickel pig iron and high carbon ferrochrome rose to the highest level since April 2015. (refer to Fig.1)

Fig. 1

As the Chinese stainless steel prices peaked out, the mills and resellers struggled to compete in the northeast Asian market. In fact, the Taiwanese domestic prices have remained the same since early August. Thus, it was expected for the Chinese prices to fall regardless of the raw material prices. What wasn’t expected, however, was during the last two weeks of December, the Chinese domestic prices and margins revived and ended the year better than November? Mills were more responsible with their production volumes than earlier in the year and the export markets have also revived and more quickly than the domestic market.

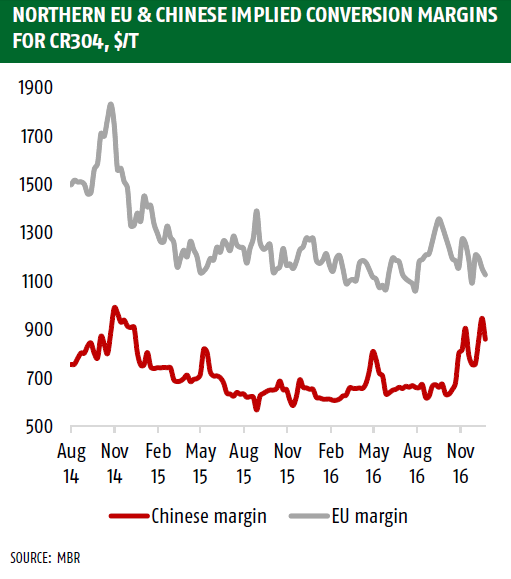

After the mid-November peak, the prices in the Chinese domestic market have risen far less acutely than their counterparts in other Asian markets. The costs have fallen, the conversion margins have increased, whereas the margins of European mills have fallen (refer to Fig. 2).

Thus, for the year as a whole, it resembles a complete recovery from the disastrous 2015 for the Chinese and Asian market.

Fig. 2

Based on past data, it is clear that China’s “real” consumption of stainless steel, which deducts for stock changes, is falling less quickly. Flat rolled inventories are retreating more than usual and the stocks of bars and rods are expected to rise.

Thus, we at Ambica Steels, believes that the improving trend of late 2016 will continue on to 2017 and it will prove to be a much better year for the Chinese and other Asian manufacturers.